{kind=link}

Name of Quantlet: PricingKernel_NonMonotone

Published in: 'Non'

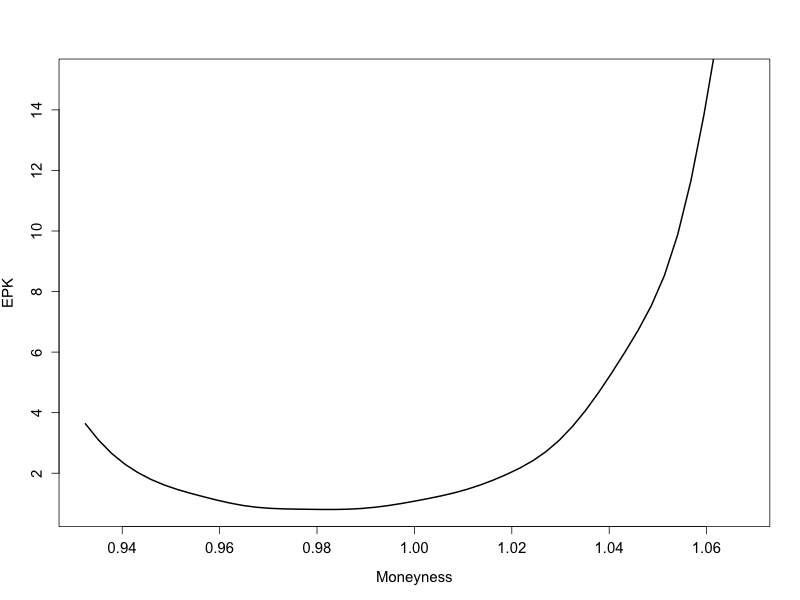

Description: 'Calculate the Pricing Kernel estimation for Crypto Currencies and SP500 options based on classical method and CDI method'

Keywords: 'Pricing kernel, R, Crypto, SP500, Option, puzzle, CDI'

Author: 'Ruting Rainy WANG; Lei Tracy ZHOU; Xiaorui ZUO'

Submitted: '17.10.2024'