{kind=link}

Name of QuantLet: 'LLM-Risk'

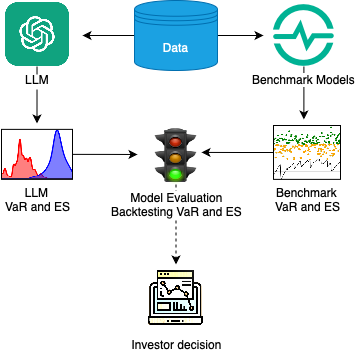

Published in: 'Financial Risk Forecasting with Large Language Models'

Description: 'Implementation of Value at Risk (VaR) and Expected Shortfall (ES) estimation using Large Language Models (LLMs) for financial time series forecasting.'

Keywords: 'Value at Risk, Expected Shortfall, Large Language Models, Financial Risk, Time Series Forecasting'

Author: 'Daniel Traian Pele'

Submitted: 'Monday, 4 November 2024'